We have been recommending, at Franc, that investors ride out the crash. Our reasons are threefold:

1.Timing the market is difficult.

2.Being out of equities when the market turns can dramatically reduce future returns.

3.Rand-cost averaging is an effective way to keep building equity exposure in a bear market.

In this article we explain these points more fully.

Crash!

If you are a young investor starting out on the journey of building wealth, the current crash in share prices may make you avoid the stock market forever. This would be a mistake.

Over the long term, equities have almost always been the best performing asset class, typically beating other options like property and fixed deposits by miles.

You'd be forgiven for questioning how that could possibly be true given what's happened on the JSE in the last two months. The index fell 11% in the last week of February. By 23 March it was 36% off its peak. It’s recovered dramatically, but at the time of writing (8 April) it’s still around 20% below its January peak.

Timing vs Time In

As we've said before in other articles, timing the market is not easy.

In theory, it would be good to wait until the market reaches its lowest point before you start investing (or resume investing).

The problem is that nobody can tell you when the market is going to reach that low point. Is it today? Was it yesterday?

(If you’re interested in a comparison of this crash and previous crashes, check out Crash Anatomy.)

If you look at graphs of previous crashes, it's easy to think you could have sold near the top and bought back in at the bottom. But hindsight is easy, knowing what to do today is a different story.

But you do want to be 'in' the market. After the 2008 crash – after the market bottomed out in March 2009 – US markets shot up 75% in a year. Getting back in late – or not getting back in at all – would have resulted in significant loss of potential gains.

It's a catch-22. On the one hand you want to be 'in' the market when the next bull run starts. On the other hand nobody can tell you with certainty when the market is at its lowest, which means you don't know when to start. Is there a way to resolve this conundrum? The answer is rand-cost averaging.

Making the bear work for you

Rand-cost averaging is the effect of continuing to invest through market cycles. If you are investing in equities every month through a stop order then you’re doing it already!

If you keep investing regularly, the average cost of your portfolio is the average of all your different purchases.

In a bear market, the result is that your cost is dropping every time you invest.

The example below illustrates exactly how this works.

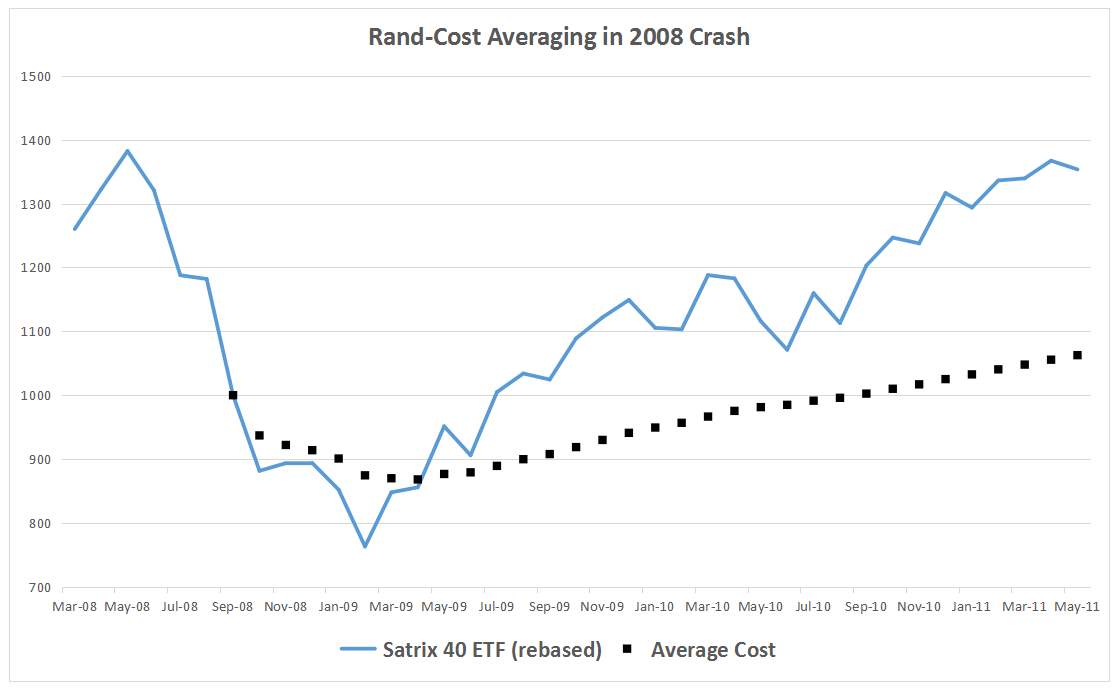

The blue line shows the actual movements of the Satrix 40 price from May 2008 to May 2011. The black dots show the average cost of investing for an investor who started putting in R1,000 a month in September. The index has been rebased so that the left axis shows rand values from a starting point of R1,000 end September.

The market had fallen about 40% – similar to the fall the JSE experienced between mid-January and mid-March 2020 – and in late September 2008 it looked like the market was ready to rally, which meant that some lump-sum investors were sucked back in too early (you can't see this in the chart below because it is only shows month-end values, but mid-September 2008 there were signs the crash was over). Let’s imagine someone called Mr Jones did this – we’ll compare rand-cost averaging with his results later.

As the chart shows R1,000, invested in September 2008 was worth R1,000. It was worth less than R900 a month later, but another R1,000 invested in October reduced the average cost of the total investment to R950 (per R1 000 invested).

This pattern continued until February 2009 – each month the value of each R1,000 previously invested was less, but the new investment reduced the average cost. At the end of April 2009, when the market began climbing, a total of R8,000 had been invested – and the value of the position was R7,900. Suddenly the investor was almost square.

After that the value of the investment kept climbing into increasingly positive territory. By December 2010 the position was worth R36,000 off an investment of R28,000 (30% up), and by June 2014 it was worth R116,000 off R70,000 invested (65% up).

As you can see, an investor who did rand-cost averaging was better off than someone who only started investing later (i.e. once the blue line was above the black dots).

Even though our black-dot investor started investing 'too early', the average cost of the position was lower than it would have been had the process only started after April 2009.

An Investment Opportunity

The chart above – which reflects what actually happened to an investor in the 2008 crash – illustrates very well why we feel that time in the market is better than trying to time the market. Rand-cost averaging and a falling market is actually an investment opportunity if you are a young investor.

Sure, if by some stroke of luck you had started investing in February 2009 rather than six months earlier, you would have enjoyed even better returns, but history teaches us that most investors miss the bottom – and the majority only start coming back to the market once the next bull run is firmly established.

And what about Mr Jones? Let’s say that he invested R10,000 in September 2008. Compare this with the black dot on the graph at June 2009 – at which point someone doing rand-cost averaging had also invested R10,000. Here’s the rub – even though the market was still down, the R10,000 invested monthly was already worth R10,300. The investor was up! Mr Jones’s R10,000, however, was only worth R9,060 – having been invested for ten months, he was still down.

The difference might not seem huge, but it gives the monthly investor a permanent advantage – that first ten thousand is forever getting more growth. By April 2011, for example, Mr Jones’s ten thousand had grown to R13,672, but the ten thousand of the monthly investor had grown to R15,551.

In short, keep investing monthly if you can, don't let the crash chase you away from a great investment opportunity.

Footnote: This article is aimed at investors who are in the early stages of building their investment portfolios. Investors approaching retirement face different challenges when the market crashes because they can't take advantage of rand-cost averaging in the same way. You can read more about that in Cash Out or Ride it Out Revisited.