In this previous article we went through the different types of retirement funds and how they work. Less than 10% of South Africans can retire comfortably - the primary reason being they just do not have enough of a capital base on retirement either because they have not been investing enough whilst working and/or they dipped into their retirement funds at some point.

We are going to focus on the second issue here - accessing your retirement pot before retirement. It is important to distinguish between investments you have earmarked for retirement (tax free savings accounts and other discretionary investments such as your Franc account) but are not formal retirement products (“Normal Investments”) and investments in pension and provident funds (“Retirement Investments”). The latter has its own rules when it comes to tax and accessibility.

Whilst I would encourage you to not access any of your Normal Investments if you really don’t need to before retirement, if you do so it would not be as detrimental to your future financial wellbeing compared to if you cash in on your Retirement Investments.

When can I have access to my Retirement Investments?

If you resign, retire or are retrenched from your employment, you are able to access your Retirement Investments. If you are retiring and will not have any access to other income then this is exactly why you have these investments so it makes total sense to start utilising them for their purpose. If you die then your Retirement Investments will go to the beneficiary you appointed (assuming the trustees agree).

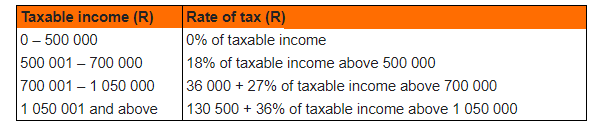

Retrenchment

The first R500,000 you cash out (together with any severance pay) is not taxed, then you start paying tax on any further amounts received. This is a once off allowance - if you get retrenched more than once it does not start from zero, you pay tax above what you have already earned in severance or accessed from your Retirement Investments.

As you can see from the table above, the tax becomes quite hefty after you have accessed R500,000. If you are retrenched and need some cash, another option would be to apply for UIF funding which could come in very handy when times are tough.

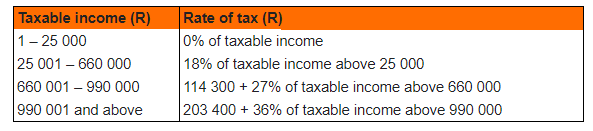

Resignation

If you resign from your employment and want to access some of your Retirement Investments, the taxes are much higher. Here, only the first R25,000 is not taxed. I guess versus retrenchment which is not really in your control, if you resign you have made the active choice to do so hence why the taxman is less sympathetic to your cause. You also don’t have the option to apply for UIF funding if you resign.

We even sometimes hear stories of people resigning from their jobs just so that they can get access to these funds before retirement. Some employers are also letting their employees resign, get access to their Retirement Investments and then reinstate them afterwards - something which is illegal!

The SA Treasury is apparently looking at ways to allow people to access a small portion of their Retirement Investments during emergency/extraordinary circumstances but any legislation is only likely to be finalised in the next year or two. It is a balancing act for the government - they want people to maximise their Retirement Investments but also can’t have people doing things like resigning just to access some of their money!

It’s worth also noting that Retirement Annuities (“RAs”) are treated differently to Pension and Provident Funds. RA funds can only be accessed once you are 55 years of age unless you are disabled, emigrating or the value of your RA is less than R15,000.

So, what's the fuss?

Well, as we harp on about a lot at Franc - Compound Growth! If you access money before retirement you are not giving this money the ability to grow. And if you are paying taxes on it, even worse! You are accessing and consuming less than what your investment is worth. Simply put, unless you have a large pool of Normal Investments (probably unlikely as if you needed money this is what you should be cashing out first!) then you will most likely not be able to retire comfortably.

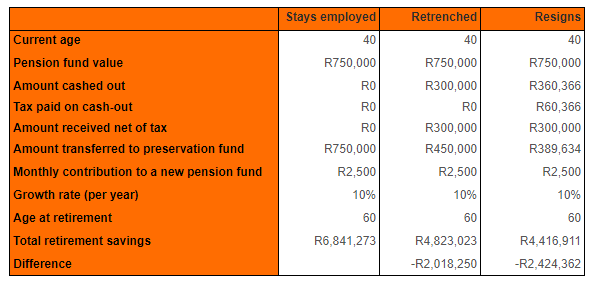

Let's look at these examples below. Here we compare 3 people all aged 40 who have left their jobs and started new ones immediately but for different reasons. The retrenched employee cashed out R300,000 (no tax) whilst the employee who resigned cashed out over R360,000 so that he could receive R300,000 after tax. The other employee left his investment untouched. They then all invested the same amount of R2500 per month for 20 years. As you can see the difference at the end is quite substantial - R2m between the retrenched person and the person who did nothing and R2.4m between the person who resigned and who did nothing. This is even before taking into account the person who did nothing can cash out their full R500,000 allowance without any tax whereas the others can’t.

The large differences in investment balance is purely due to the fact that the retrenched person had R300,000 less to grow for 20 years and the person who resigned had R360,000 less to grow for the period.

As you can see the differences can be very large so please try to avoid accessing your retirement funds unless it is really a last resort! Be part of the 10% that can retire comfortably! R4.8m and R4.4m may seem like a lot of money now, but remember inflation means that in 20 years it will be worth a lot less - R4.4m in 20 years is worth R1.7m today assuming a 5% inflation rate and R1.7m today will just about buy you an R11,000 monthly pension as a 60 year old male.